SEARCH OVER 12,000 NEW LEASING DEALS

Business Car Leasing - Company Car 2026/27 Tax Changes

How does it work?

In simple terms, if you provide your employees with company cars that are available for personal use, HMRC classes the car as a non-cash benefit - similar to other benefits like private medical cover. As a result, the employee becomes liable for a tax charge. That charge is known as Benefit-in-Kind (BiK).

For further information read on below, or if you have more specific questions, get in touch with the team.

P11D Value

The P11D is a form HMRC requires all employers to complete. It details the cash equivalent values of all benefits and expenses provided during the tax year.

The P11D value of a car is the starting point for calculating company car tax and is worked out as follows:

Vehicle List Price (inc. VAT)* + List Price of any Accessories (inc. VAT)** + Delivery Charges − Any Capital Contributions made by the employee = P11D Value

* This value excludes any First Year Registration fee and Vehicle Excise Duty (VED).

** Accessories added at a future date must be added to the P11D value if they cost £100 or more. Accessories costing less than £100 are excluded, and like-for-like replacement accessories will not amend the P11D value.

The value of the benefit is calculated as follows:

P11D Value × CO2-derived Appropriate Taxable Percentage (per CO2 table) = Benefit-in-Kind

Diesel Supplement

If a car runs solely on diesel, a 4% supplement is added to the appropriate taxable percentage, subject to a maximum of 37%. The supplement does not apply if the vehicle meets the Real Driving Emissions Step 2 (RDE2) standard.

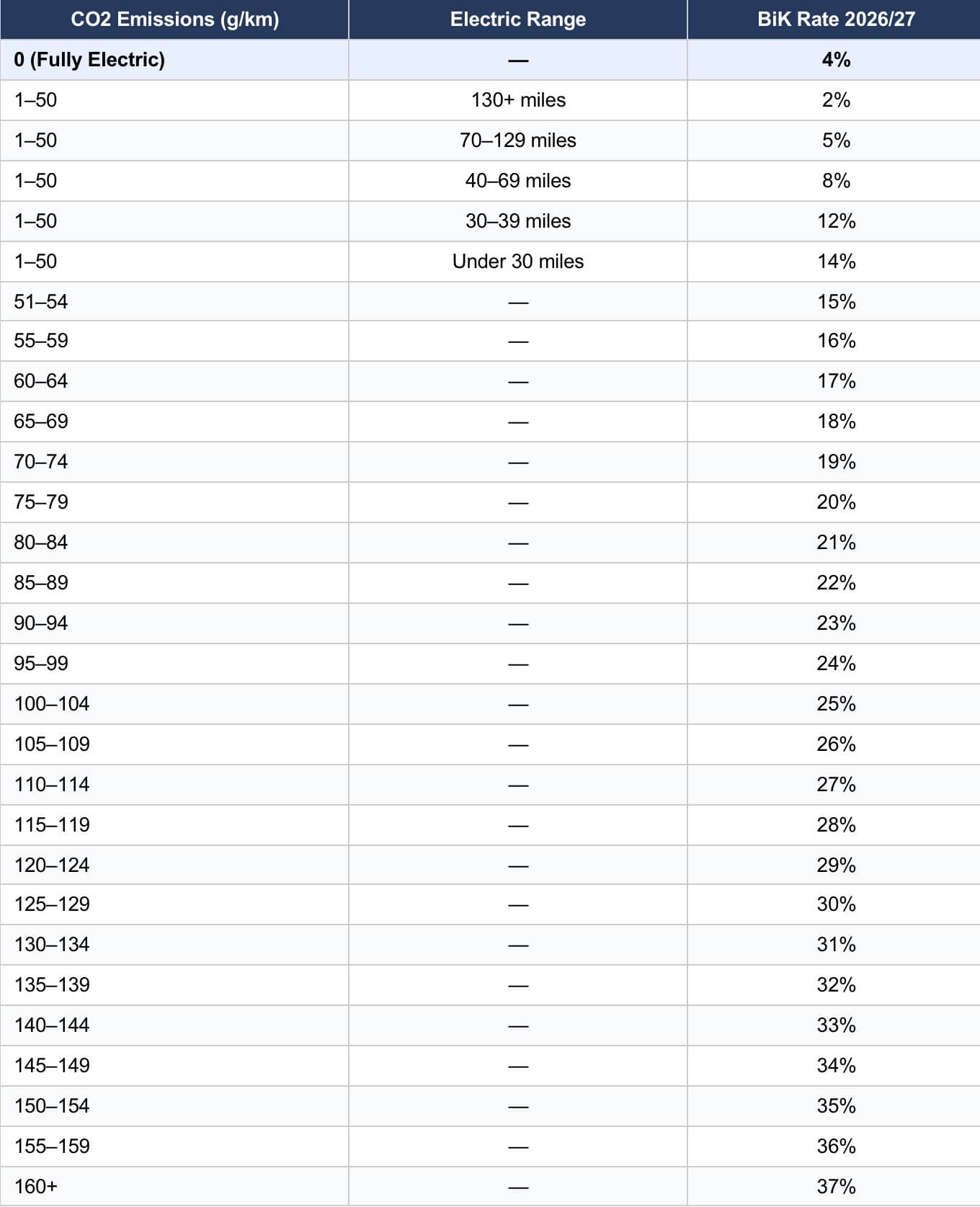

Cars Registered FROM 6 April 2020 - Appropriate Taxable Percentage (2026/27)

What’s changed for 2026/27?

The most notable update from 6 April 2026 is the increase in the BiK rate for fully electric company cars, which has risen from 3% to 4%. This forms part of the government’s pre announced annual escalator for zero emission vehicles.

Rates for all other vehicles have also increased by 1 percentage point, in line with the same escalator, up to the 37% maximum.

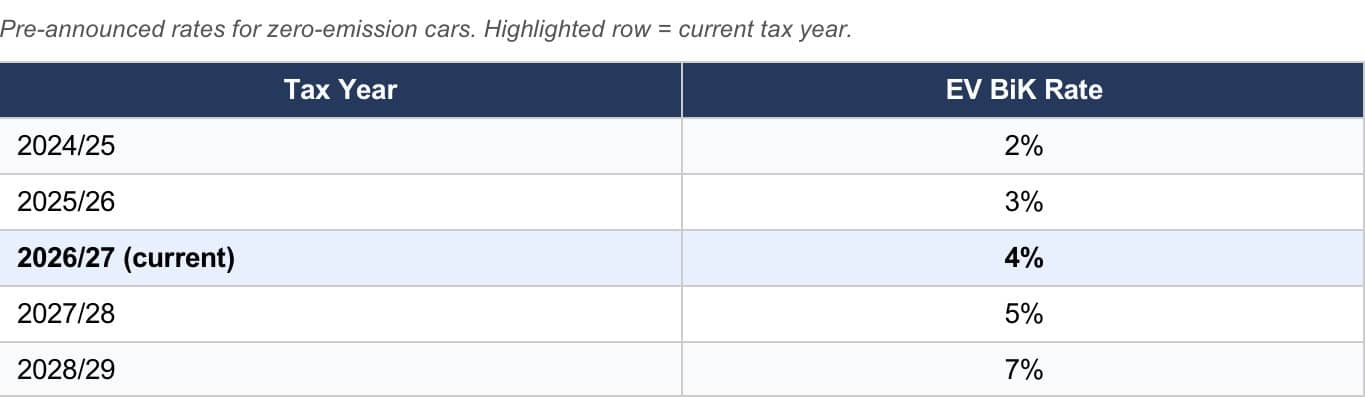

Confirmed future rates for electric vehicles:

Source - HMRC.

Even with these gradual increases, electric cars remain significantly more tax-efficient than petrol or diesel alternatives, which can attract rates of up to 37%.

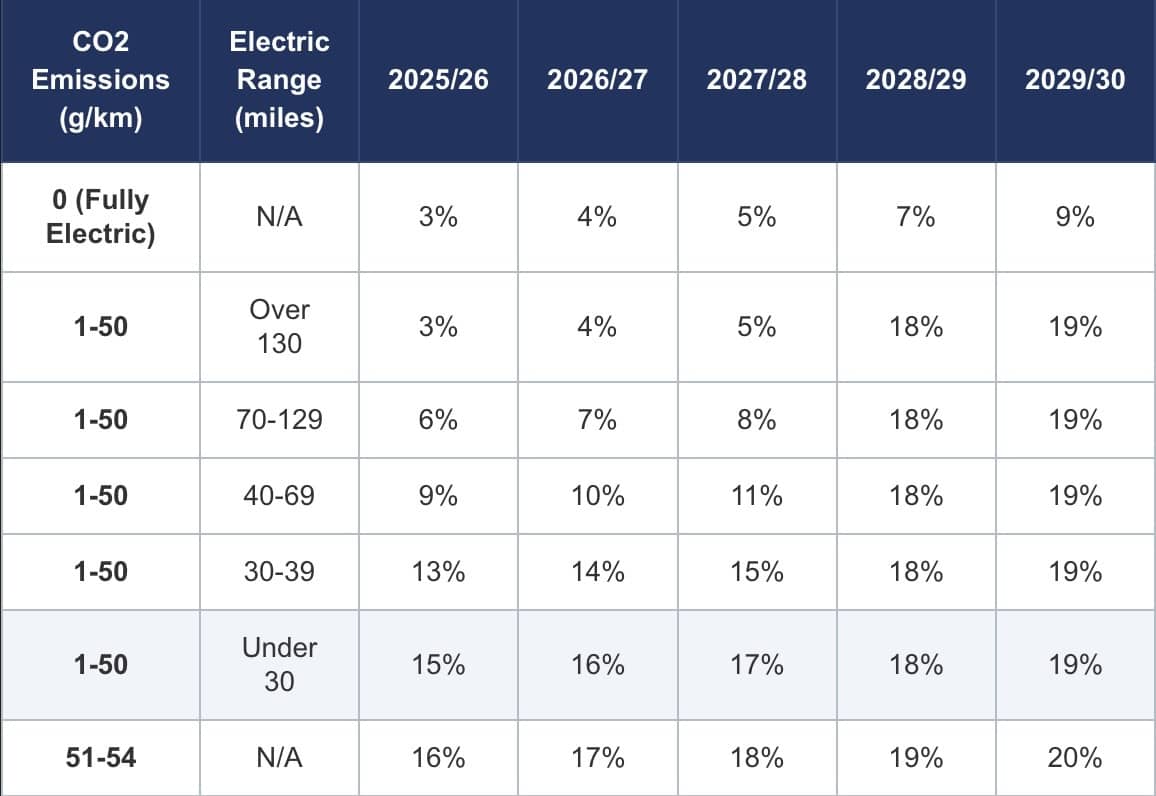

A note on plug-in hybrids (PHEVs) from April 2026

From April 2026, all new plug in hybrid vehicles must be tested and certified under the new Euro 6e-bis emissions standard. This standard uses a more rigorous test cycle that better reflects real world driving - and as a result, many PHEVs will carry higher official CO2 figures than under the previous test.

Because BiK rates are based on official CO2 figures, this change may increase the taxable percentage for some PHEV models. The government has introduced a two year easement (April 2026 to April 2028) to help businesses and fleet operators adjust, but it is worth factoring this into any new lease decisions involving plug in hybrids.

All CO2 emission figures can be found within the product description of all vehicles on our website.

If you have questions about how this affects your fleet, our team can help - don't hesitate to contact us.

The BiK value is then adjusted for any of the following:

1. Part year - when the car was not made available until part way through a tax year, or ceased to be available part way through a tax year.

2. Period of unavailability - when the car was unavailable for a minimum consecutive period of 30 days or more.

3. Employee payments for private use - any contributions the employee makes specifically for private use of the car.

4. Shared use - periods when the car has had shared use between employees.

The final adjusted BiK value is then multiplied by the employee’s marginal tax rate to determine the tax payable.

What does the employer pay?

For employers, the BiK value is used to calculate Class 1A National Insurance contributions - the amount the employer pays on the benefit provided to the employee. From April 2026, the Class 1A NIC rate is 15%.

A practical example

To illustrate how this works, here is an example using a £40,000 fully electric company car in the 2026/27 tax year:

∙ P11D value: £40,000

∙ BiK rate (2026/27): 4%

∙ Taxable benefit: £1,600

∙ Tax payable (basic rate, 20%): £320 per year / approx. £27 per month

∙ Tax payable (higher rate, 40%): £640 per year / approx. £53 per month

∙ Employer Class 1A NIC (15%): £240 per year

For comparison, the same car attracted a £240/year basic rate tax bill in 2025/26 at 3% BiK - so the increase is real but modest. A petrol car with the same list price at 37% BiK would generate a taxable benefit of £14,800 and a basic rate tax bill of £2,960 per year.

We have a wide range of amazing lease deals on electric cars here at LetsTalk Leasing, which also bring amazing tax benefits.

LetsTalk Leasing can provide independent, impartial advice on car and van Benefit in Kind for your business. Please get in touch with any specific enquiries - we are available on 0330 056 3331 or via email at [email protected].

All rates on this page apply to the 2026/27 tax year (6 April 2026 to 5 April 2027). Tax rates and thresholds are set by HMRC and are subject to change. We recommend speaking to a qualified accountant or tax adviser for advice specific to your circumstances.

LATEST CONTRACT HIRE AND LEASING NEWS

Keep up to date with the latest leasing news, reviews and advice.

Audi Leasing vs PCP: What's the Difference?

9th Jul 2026

Not sure whether to lease or PCP your next Audi? We break down the key differences in ownership, cost and flexibility to...

Best Audi lease deals for under £500 a month in 2026

29th Jun 2026

Combining premium comfort, cutting-edge technology, and chic styling, it’s easy to understand why Audi is among the UK’s...

What to expect when your Audi lease ends

29th Jun 2026

In this article, we identify your options are after your Audi lease ends, how the end-of-lease inspection works, and wha...